Mastering Interchange: What Every Business Should Know About Card Payments

When you swipe your card to make a purchase, an invisible world of transactions and fees kicks into action. One major player in this hidden flow is the interchange fee.

Let’s dive into what interchange is, how it works, and what factors influence interchange rates, complete with helpful diagrams.

What is Interchange?

Interchange refers to the fee paid by merchants to the card-issuing bank every time a consumer makes a card payment. It compensates the bank for risks involved in approving the payment, costs related to fraud, bad debt and handling of the transaction.

Example:

A consumer swipes a Neobank card to buy $100 worth of goods.

$2.50 goes to the issuing bank (interchange fee).

$0.50 goes to the acquiring bank (acquiring fee).

The merchant ultimately receives $97.

Factors That Impact Interchange Rates

Several elements influence how much interchange a merchant pays:

1. Credit vs. Debit

Credit card transactions usually carry higher interchange rates compared to debit cards.

2. Rewards Programs

Cards offering cashback, airline miles, or other perks often have higher interchange fees to fund these rewards.

3. Online vs. Offline

E-commerce (online) transactions face higher interchange rates than Point-of-Sale (offline) transactions due to increased fraud risk.

4. Consumer vs. Commercial

Corporate cards used for business expenses generally have higher interchange fees than personal cards.

5. Merchant Category Code (MCC)

Different merchant types (grocery store vs. gas station) have different interchange rates based on their MCC.

6. The Card Network

Visa and Mastercard typically have lower fees, while American Express often charges higher rates.

7. Network Partner Programs

Some big retailers negotiate lower interchange rates through partner programs with Visa and Mastercard.

8. Size of the Issuing Bank (U.S. Only)

Thanks to the Durbin Amendment, large banks face capped interchange rates on debit cards, but smaller banks can charge higher fees, benefiting partnerships with FinTechs.

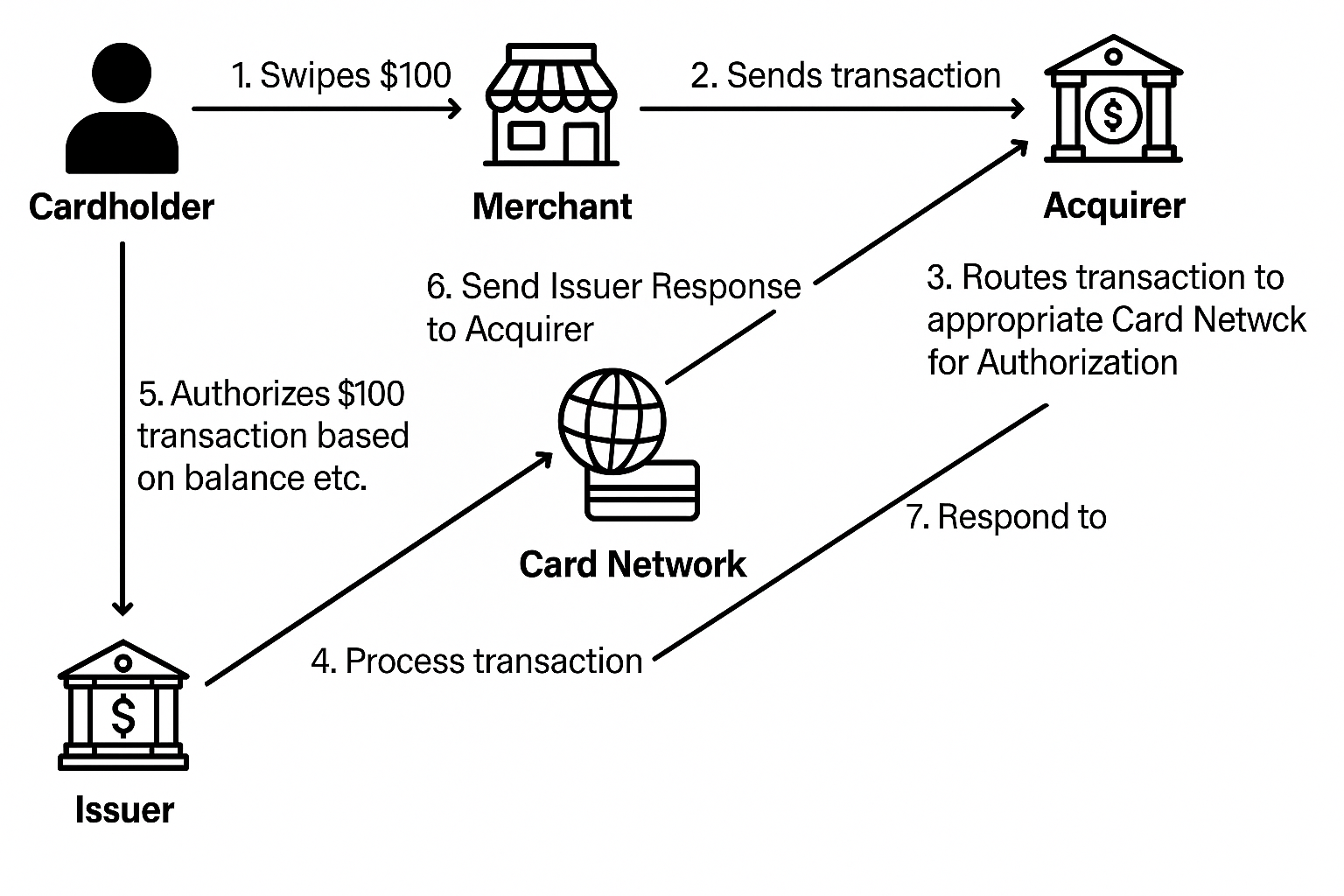

The Transaction Flow Explained

Here’s a simple breakdown of how a card purchase happens:

Purchase Authorization Flow

Cardholder swipes card ($100).

Merchant sends transaction to Acquirer.

Acquirer sends the transaction to Card Network.

Card Network forwards it to the Issuer.

Issuer checks funds and authorizes $100, places a hold.

Issuer sends approval back to Card Network.

Card Network forwards it to Acquirer.

Acquirer notifies Merchant: Purchase Complete.

Diagram: Authorization Flow

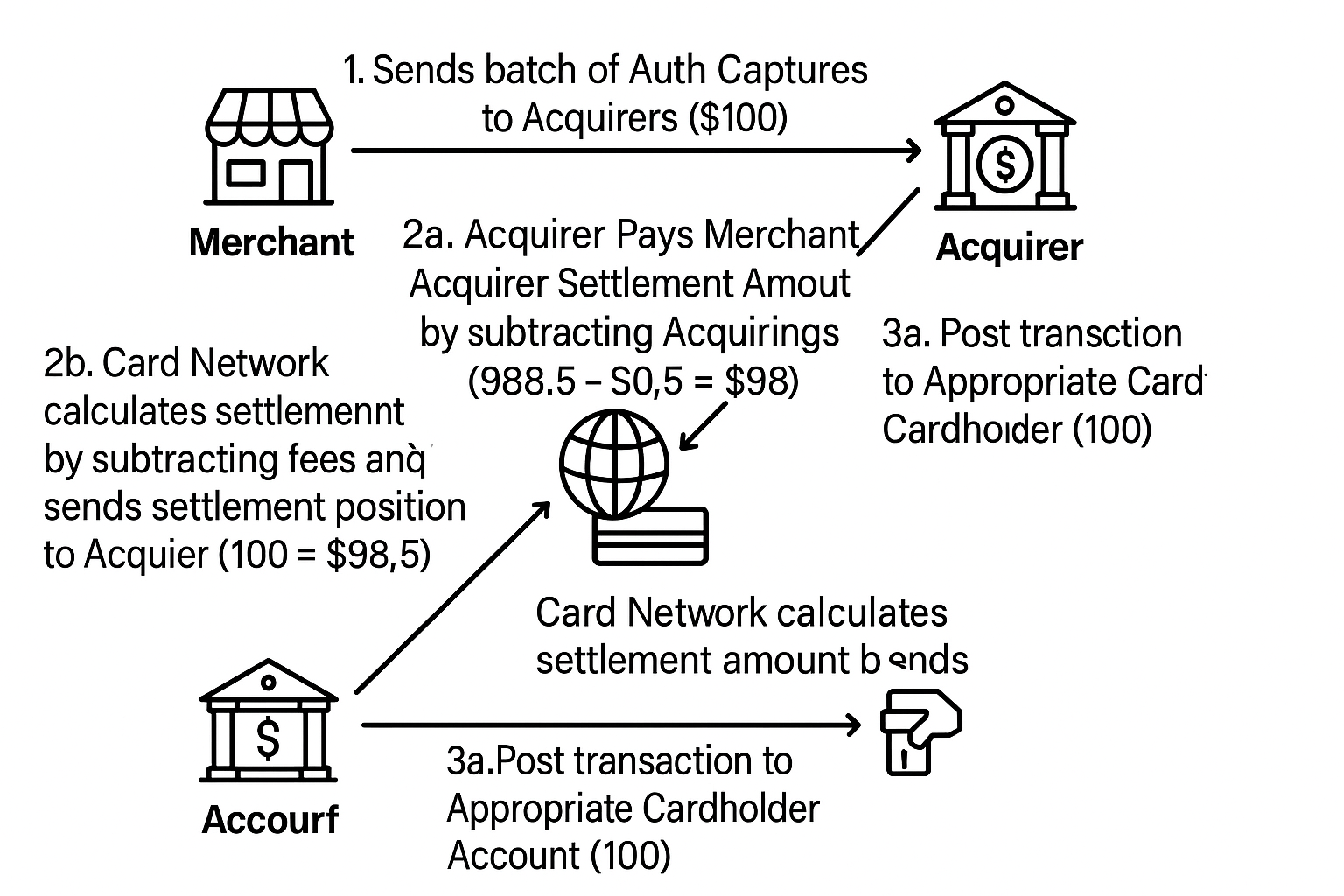

Purchase Clearing and Settlement Flow

Merchant sends batches of captured transactions to Acquirer ($100).

2b. Acquirer pays Merchant $97 (after acquiring fee deduction).

Issuer posts $100 transaction to Cardholder’s account.

Diagram: Clearing and Settlement

Why Interchange Matters

Understanding interchange is crucial for merchants, payment providers, and FinTech companies. It’s not just a “cost of doing business” but a negotiable and optimizable expense that affects profitability.

By comprehending the flow and the influencing factors, businesses can better navigate the payment landscape, optimize costs, and make strategic partnerships.

Other Fees Related to Card Processing

Besides interchange, there are several additional fees that merchants should be aware of:

Payment Gateway Fees

Charged by the technology provider that securely transmits card data from the merchant to the acquirer.

PCI Compliance Fees

A monthly or annual fee to ensure that the merchant adheres to Payment Card Industry Data Security Standards (PCI DSS).

Chargeback Fees

Fees incurred when a customer disputes a charge and the transaction is reversed.

Monthly Minimum Fees

If a merchant does not meet a minimum processing volume, they might be charged an additional fee.

Cross-Border Fees

Additional charges when the card used is issued by a bank in a different country than the merchant.

Early Termination Fees

Penalties charged if a merchant ends their card processing contract early.

Assessment Charges (Scheme Fees)

These are fees charged by the card networks (Visa, Mastercard, etc.) for using their payment network. They are usually a small percentage of each transaction and are separate from interchange and acquiring fees.

Do follow us on Instagram and LinkedIn for more payment related contents.

Want to learn more about interchange rates for your business? Use our interactive interchange calculator to understand payment processing fees for your business!